Everyone Deserves a Fresh Start

1300 796 850

Apply For Finance

Loan Saver Network Blog Posts

Tax Debts

Managing Tax, PAYG and GST Payments

Managing Tax Debts

When To Use Tax Debt Mortgage

How ATO Views Tax Debts

ATO Payment Plans

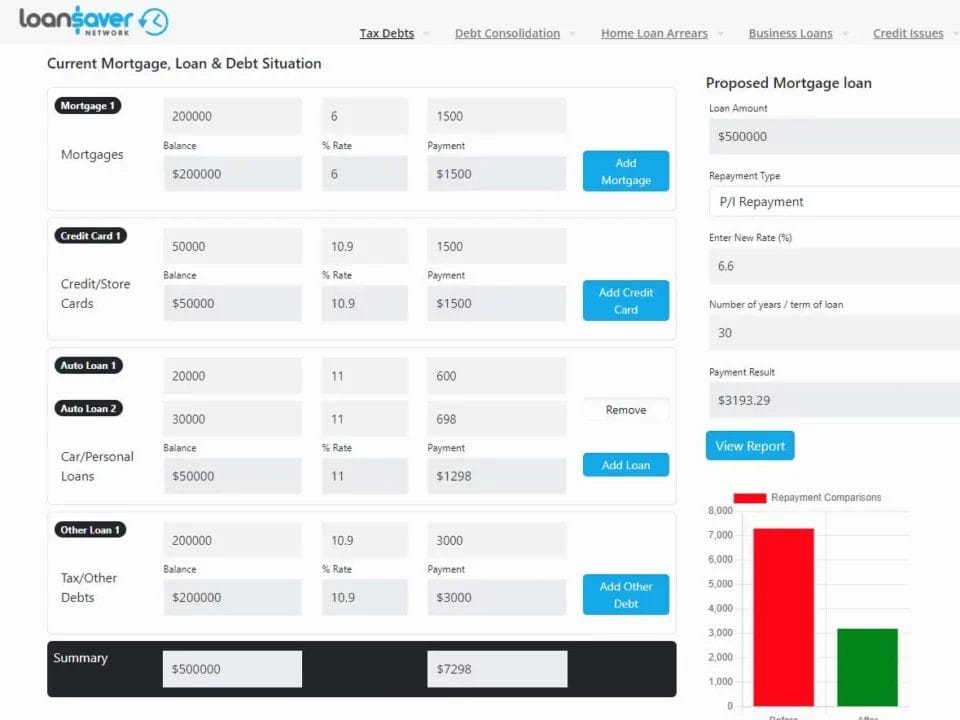

Tax Debt Consolidation Loan Calculator

Benefits Of A Calculator

Tax Debt Case Study – Warren

Debt Consolidation

How to Consolidate Part 9 Debt Agreements?

Debt Agreements and Buying a House

Credit Card Debt

Common Reasons For Debt

Three Reasons To Consolidate Your Debts

Best Times To Consolidate Debt

Facts and Case Study

Home Loan Arrears

Mortgage Arrears Causes

What You Need To Know

Mortgage Arrears Questions

Arrears Case Study

Mortgage Arrears Process

Business Loans

Business Loans Comparison

Caveat Loans

Vehicle Caveat Loans

Second Mortgages

Unsecured Business Finance

Credit Issues

Frequently Asked Questions

Credit Scores

Credit Defaults

Court Judgements

Mortgage Arrears

Part 9 Debt Agreement

Personal Insolvency Agreement (PIA)

Avoiding Receivership

Voluntary Administration

Liquidation Explained

Is Personal Bankruptcy suitable for me?

Contact

About Us

Privacy

✕

Loan Saver Network Blog Posts

Home

Loan Saver Network Blog Posts

Published by

Colin

Why Do I Owe the ATO Money & What to Do About It?

Published by

Colin

Benefits of a Debt Consolidation Calculator

Published by

Colin

Mortgage Stress: Are you pressured by inflation & increasing interest rates?

h3

date

DESC

10

masonry

3

images-only

date

DESC

Apply For Finance

Loan Saver Network Blog Posts