April 24, 2018

Banking Royal Commission and Lender Assessment Changes The Banking Royal Commission is certainly causing waves in lending circles which we feel will have a wide spread […]

April 23, 2018

June 9, 2015

June 9, 2015

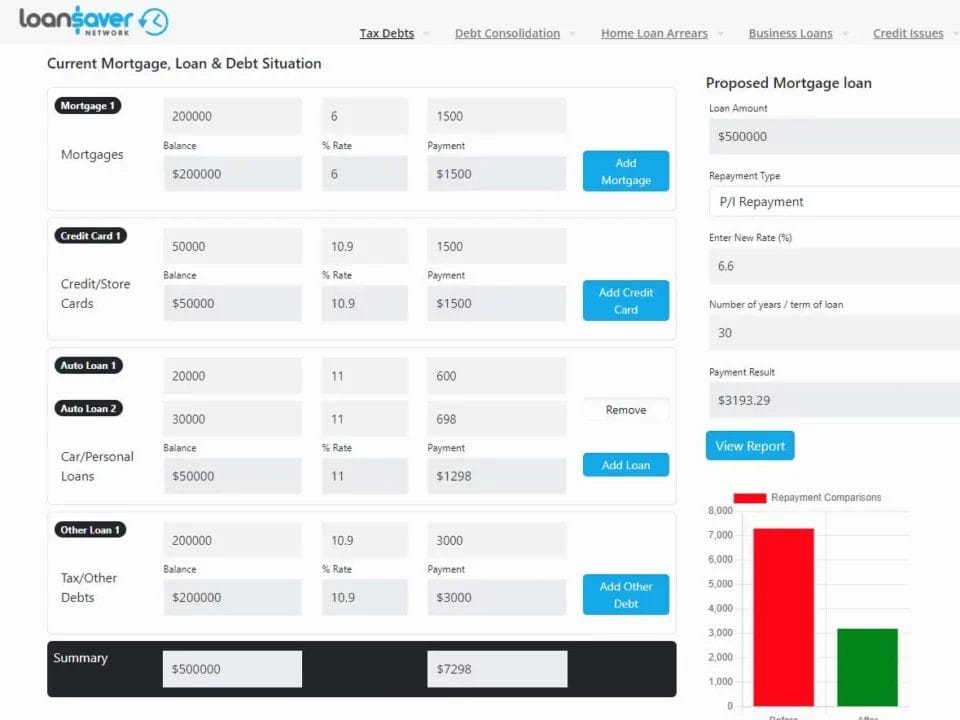

Benefits of using a Mortgage Calculator A mortgage calculator can be crucial for people who are home buyers however what are the benefits of using a […]

June 9, 2015

{kind=link}

{kind=link}

The ATO, Covid, and Tax Debt Covid, the pandemic and the government response have been cited as the biggest social upheaval since the second world war. […]

June 9, 2015

A Real-Life Example of Debt Consolidation Is Debt Consolidation Worthwhile? A lot of us have heard the words Debt Consolidation, but are confused about what they […]

June 9, 2015

June 8, 2015

. Solutions For Managing BAS and PAYG Payments At Loan Saver Network, we speak to many businesses regarding their tax obligations. As such, we gain a […]

July 4, 2014

Invariably most small or even large businesses need to obtain a payment plan for a tax debt, BAS, or other debt from the ATO at some stage. […]

May 21, 2014

h3

date

DESC

10

masonry

3

images-only

date

DESC